Featured

Table of Contents

Access practical services and helpful details to help you take control of your credit report, and much better secure yourself from identity theft and fraud.

Raising your credit history can help you unlock to better financial opportunities. The higher your ratings, the more gain access to you'll need to the most favorable and least expensive borrowing choices. And, beyond assisting you certify for loans, excellent credit can likewise lower barriers to other financial goalslike leasing an apartment or condo or securing lower insurance rates.

Constructing the Knowledge Needed for a 2026 Home PurchaseCredit rating of 740 to 799 are great, and ratings 800 and above are thought about excellent. If you're ready to dedicate to enhancing your credit in 2026, here are 26 ways to do it. If you're bring balances that you have actually been having a hard time paying off, you could utilize any windfalls that you receive this season to take a portion out of your financial obligation.

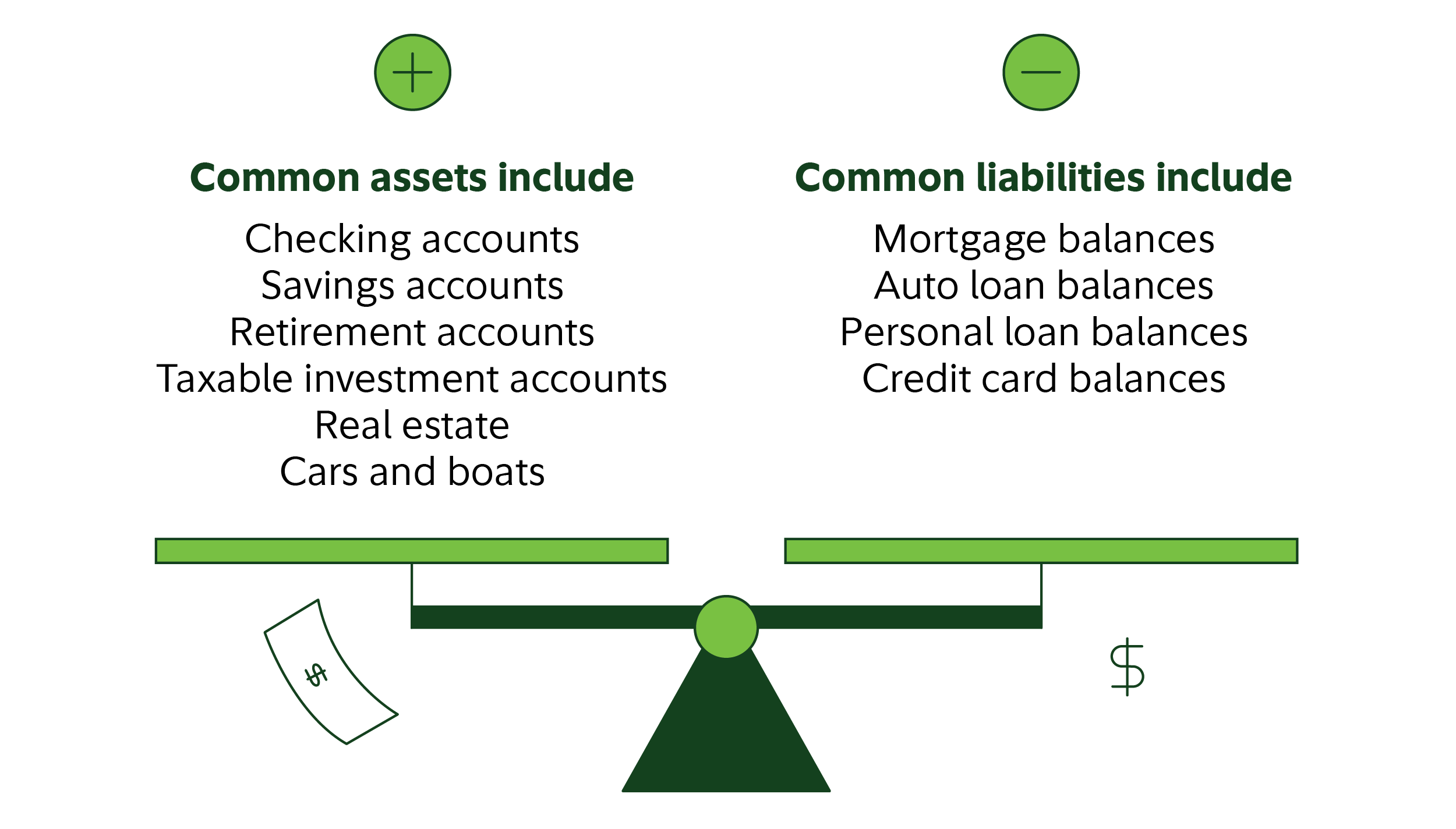

Consolidating Personal Debt for Better Financial Health

The very best way to avoid missing a regular monthly loan or credit card payment is to put your bills on autopay. Make certain you have sufficient money in your bank account to cover each expense to avoid an overdraft. When you understand you will not need to handle a sudden rating dip after a forgotten costs, you can focus on other ways to enhance credit.

Make it a goal to lower any high-interest charge card debt first, since that likely expenses you more money in interest than, say, an auto loan or federal student loan does. Reducing your credit card balances likewise reveals prospective lending institutions that you're accountable with credit. When your credit usage techniques and climbs above 30% of your credit line, it tends to have a greater negative result on your ratings; those with the highest credit ratings typically have an usage rate in the single digits.

If you're concentrated on constructing credit from scratch or recuperating after a hit to your rating, a credit-builder loan from a credit union might help. You'll make fixed payments for 6 to 24 months, and your cash will being in a cost savings account you'll be able to gain access to at the end of the loan term.

Can Better Financial Habits Improve Your 2026?

Just make sure the loan provider reports to all 3 credit bureaus (Experian, TransUnion and Equifax) for the finest credit-building chance. This type of credit card requires a money deposit, normally around $200, which becomes your credit limitation.

After you've developed a history of using your protected card responsibly, your card issuer might upgrade you to an unsecured card down the line. You can likewise improve credit by joining a trusted household member's or buddy's charge card account as an authorized user. You'll have the ability to utilize the card to make purchases, and the card's payment history will reveal up on your credit report.

Work with the primary cardholder to pay them for your purchases, as they'll be ultimately responsible for any balance on the card. Examine them each carefully.

Fixing any issues might provide your credit scores a lift. lets you include eligible lease, phone, utility, insurance and streaming payments to your credit report. That, in turn, may cause your FICO Rating to rise. For an expense to be qualified, you'll require to have at least 3 payments in the previous 6 months (including one payment within the past three months).

Those who are qualified might see an instant increase to their FICO Score. Even if you no longer use an old charge card, it's normally best to keep the account open. That's since your credit rating benefit from a long credit rating and a high overall credit limit. Closing established accounts will reduce the average age of your accounts and lower your overall credit line.

Actionable Steps for Reducing High-Interest Debt

If a charge card comes with a high annual cost you can't pay for, closing the account might be a great optionor ask your provider to downgrade the card to a no-fee version if possible. When you get a brand-new credit card or loan, a hard query will appear on your credit report, possibly leading to a little, short-lived dip in your scores.

Lots of difficult questions in a short time might be an indication to loan providers that you're searching for lines of credit you will not be able to pay. Strategic debtors, however, will use for a few loans of the exact same typesuch as a home loan, vehicle or individual loanto compare rates.

Keep in mind, however, that the scoring models do not provide this exact same allowance for credit card applications; all of these will count separately regardless of when you submit them. In addition to lowering existing financial obligation balances, decrease ongoing debt by making it an objective to pay off your credit cards each month.

Consolidating Consumer Liability for Total Financial Health

When you monitor your credit score, you can intervene quickly if it drops. You can resolve factors that influence your rating, such as high balances, late payments or too many recent hard questions., including through your existing credit card provider or bank, or through Experian.

To assist keep your information safe, use a password supervisor to create and keep distinct passwords and avoid making monetary transactions on public Wi-Fi networks, which could be susceptible to hackers. Lenders look for a mix of accounts in your credit file to show that you can manage multiple types of credit.

Constructing the Knowledge Needed for a 2026 Home PurchaseIf you just have one type of credit in your file, including something different could enhance your credit mix. But while credit mix accounts for 10% of your FICO Rating, you should not apply for new charge account just to enhance your score. That could put you at risk of handling financial obligation you can't pay back.

{kind=link}

Latest Posts

Achieving Budget Freedom through Expert Planning

Top Performing Financial Wellness Tools for 2026

Using Digital Tools for Better Financial Wellness